April 1, 2004

Canarc Resource Corp: Ready for Launch?

Eric Hommelberg

April 12, 2004

When I wrote my piece "2003 - Year of the Juniors" in December of 2002 I said:

"Profits of 100% to more than 1000% are in the pipeline next year if invested in high quality junior exploration companies!"

Well, looking back now at 2003 all I can say is that fortunately that's exactly what happened, many Juniors appreciated by a stellar performance gain of several hundred percent during last year which is described in detail in my piece "Juniors are paying off" November 2003. OK, fine you'll say, that was 2003, but what about 2004? Too late to get on board? Has the bull market in Gold ended yet? Or has it hardly begun? Do the Junior shares still represent a great investment opportunity? Why has the Junior Exploration sector been hit so hard during Q1 2004? Was it all Hype after all or just a normal healthy correction? Does a healthy correction justify a 50% loss on my Junior Gold shares? Can it happen again? What shall we do? Well, lots of questions which beg serious answers! In order to answer those questions we'll have to examine first the current status of the two major pillars supporting the junior mining companies that in my opinion are:

- Gold Price

- Declining Gold reserves

Gold Price:

Rising Gold prices will lift the entire Gold sector. We just saw that happening during 2001 - 2003. Higher Gold prices leads to higher Gold share valuations and vice versa. Due to the greater volatility of junior mining stocks they tend to rise faster during a bull-run and tend to drop faster during a correction. A good example is the latest correction of Q1 2004. While Newmont shares dropped less than 20%, many junior miners dropped by 50% or even more. Well, that certainly hurts and I can imagine that this isn't exactly your definition of an once in your lifetime investment opportunity!

Although I didn't had the intention to include this flash-back on Q1 2004 I thought it would be useful to visualize the recent correction and its impact on the long-term trend. In order to do so we'll take a look at the long-term chart of the HUI first.

As you will see, during the three-year bull market in Gold, gold shares do correct every now and then which is of course normal and inevitable. Sometimes they experience a minor correction sometimes a major one. You'll notice that the major corrections do occur when the Gold shares moved too far ahead from their 200 dma and tend to bottom near or at the 200 dma line.

So whenever a Gold Stock moved too far away from its 200 dma and get over-extended gravity will pull it back. No single stock ever managed to escape gravity from the 200 dma permanently. Fortunately those major corrections do not happen very often (last time it happened before this correction was March 2003) but unfortunately these sell-offs do scare lots of investors out of their Gold stocks. To those investors I would say "don't be scared for a major correction to the 200 dma because it's almost inevitable and is just a (although a painful one) typical characteristic of a bull market at work. It happened in July 2002, it happened in March 2003, it happened in March 2004 and it will happen again."

The good news however is that once such a painful correction is over the odds are a steady upward trend will commence for a relative long period (>6 month) without any significant setback. In other words, History tells us that the best buying opportunities occurs near or at the 200 dma.

Adam Hamilton (Zealllc.com) told his readers recently:

"As a matter of fact, I believe that another legendary buying opportunity is rapidly approaching in gold stocks. In the just-published March issue of our acclaimed Zeal Intelligence monthly newsletter, I discussed the convergence of the key technical signs leading towards this coming strong-buy signal in detail. While not quite there yet, we are getting closer every day and an amazing buying opportunity for both investors and speculators looms on the horizon."

Jim Sinclair (JSMineset.com) told his readers something similar:

"Kenny and I nailed the 1968 to 1980 market and maybe by God's Grace we will be able to do it again. This is so important because if you had this information for example in the big tech bull - knowing when the normal time outs come and when the top forms - consider what it would have meant to you. So I am quite excited to see how this gold price reaction rolls out to completion both in time sequence and in form.

We are approaching the "Window of Opportunity" for the resumption of the upside in the gold market. I can't state strong enough how important it is that gold actually performs within this period of time as that would confirm the validity of very long term proprietary studies. In terms of timing, KA and I see us as being only days away from being vindicated in our positive outlook toward both gold shares and gold."

END.

Conclusion: As long as the bull market in Gold continues great buying opportunities lie ahead whenever Gold shares do correct to their 200 dma.

So the big question remains:

"Has the bull market in Gold ended yet or has it hardly started?"

In my opinion the price of Gold still has a long way to go for reasons well documented in my report "Gold Drivers 2004" which can be found here.

Some Expert notes confirming the current bull run in Gold:

Jim Sinclair: I am a "believer" in the magnitude of the gold move that started at $342 and has had, as I have said often, a $480 plus number on it from the day it started.

Richard Russell: In the meantime, Russell advises subscribers to hold cash and gold, which, at $400 an ounce, is "as cheap as dirt." Eventually, he sees the yellow metal topping $1,000 an ounce -- and the Industrials and Transports plummeting. For this Dow Theorist, it's the perfect set-up -- for the next bull market.

Jim Puplava: The bull market in gold and silver has barely begun. It is still in its infancy as gold and silver move into their rightful role as real money. (read)

Pierre Lassonde: Newmont president, Pierre Lassonde, is certain that the gold bull market remains in its infancy, and points investors to the 1970s to understand how events might unfold in gold's favour in an era of a "manic depressive dollar."

"We haven't even started to correct the US financial imbalance of the last three years. Don't tell me that the gold bull market is over. It has hardly even started," Lassonde told the audience at the 2004 BMO Nesbitt Burns Global Resources Conference in Tampa, Florida. (read)

Conclusion: Gold Shares do represent a great buying opportunity right now!

Declining Gold Reserves:In my piece "Declining Gold reserves benefit Juniors" April 2003 I wrote: The gold Industry faces a tremendous challenge. Gold reserves are running dry coming years and not enough funding has been taken place for sufficient Exploration in order to replace existing Gold reserves. It takes at least a couple of years of exploration in order to find new Gold reserves. After a discovery, it takes another 5 to 8 years to bring the property into production. So big mining companies are facing fewer Gold reserves coming years which leads to fewer ounces of Gold reserves per share. Adding Gold reserves by means of acquisition inevitably leads to the same result, fewer ounces of Gold reserves per share. This works as an unwanted gravity which pulls the share price of the company down. Eventually the big companies will turn to the better Junior Exploration Companies in order to help find new Gold reserves. So from an investor's point of view it makes more sense to invest in Junior Companies which are increasing their Gold reserves substantially than investing your money in big companies which are facing a decline in Gold reserves and thus a decline in valuation. Let's repeat one sentence:

"So big mining companies are facing fewer Gold reserves in coming years which leads to fewer ounces of Gold reserves per share."

That was April of last year! So where are we now? Did the ounces of Gold reserves per share actually declined?

Well, the answer is yes! This is exactly what happened. Gold production per share for the Majors such as Newmont, Barrick and AngloGold have fallen from 6.4 ounces per share in 2000 to 4.2 ounces per share in 2003.

Few Headlines regarding declining Gold productionBarrick Gold Production 10% lower in 2004

NEW YORK -- Barrick Gold's [ABX] low-profile chief executive, Greg Wilkins, today told attendees of the Merrill Lynch mining conference in Toronto that production will be 10% lower in 2004. A fund manager with intimate knowledge of Goldstrike describes it as Barrick's flagship asset and says the trends have been disturbing for several years. Grade has been falling precipitously, aggravated by lower recoveries that resulted in steadily declining gold output.

AngloGold saw reserves fall by 9.2-m ounces last year

Thursday February 12, 2004

AngloGold's Geologists failed to replace all the ounces it produced last year.

Ashanti Announces Gold Production Lower Than Forecast

Monday February 16, 2004

SA gold output 4,9% lower in 2003.

Tuesday March 2, 2004

Gap in Gold Production Looming

Friday March 12, 8:10 pm ET

RENO, NV--(MARKET WIRE)--Mar 12, 2004 -- AXcess News (www.axcessnews.com) released a story highlighting gold mining companies that are having a banner year. The story points out how there is a gap in gold production looming and that investors should be watching these stocks more closely to see which companies will be outperforming their peers.

Harmony Gold cuts production by 6%

Friday April 2, 2004

JOHANNESBURG (Mineweb.com) -- Harmony Gold has finally given in to the pressures of the stronger rand, announcing today that it was considering cutting 5,000 jobs and 6 percent of its production at loss making South African operations, in an effort to widen its operating margins.

END.

You think shareholders will be cheering a declining Gold production in a rising Gold environment? No, of course not, so the pressure on the senior Gold producers will be huge in order to replace their dwindling Gold reserves. It's not only a matter of satisfying shareholder demand but also a matter of survival. In his latest Essay "Open the Checkbooks - Buy the ounces" Jim Puplava of Financial Sense Online quoted Geologist H.R. Bullis who said:

"It is no longer a question of finding ounces anymore. It has become a question of survival. According to geologist H.R. Bullis, today's VLGP's are unlikely to survive at current production rates over the next decade. It is time to open the checkbooks and go get the ounces." So from an Investor's point of view it makes sense to invest in high quality junior exploration companies which are on the verge of discovery. We're entering a time where discoveries will be rewarded tremendously. A good example we saw on Feb 26 when Victoria Resources (CDNX:VIT) announced good drill results. The company was trading at 0.99 CAD$/share at that time. Next morning its share price took off by 100% and never looked back!

So what do you think? Are the Senior Producers waking up? Are they going after new Gold Deposits? Well, it seems they are!

On Jan 27 Barrick announced that they had opened a new office in Vancouver in order to monitor junior exploration projects.

Barrick Gold's New Office Tracks Junior Exploration Cos. "Barrick Gold Corp. (NYSE:ABX) has opened a Vancouver office to monitor junior exploration projects, executive vice-president Alex Davidson said at an exploration conference. Davidson said two or three employees in the office are tracking junior projects, and visiting managers of companies and their exploration sites. The local office also handles Barrick's exploration efforts around Eskay Creek, its 100%-owned gold mine in northern B.C."

AngloGold CEO Bobby Godsell recently said:

"It is the end of big picture gold consolidation; there is no compelling logic to combining anymore. The real challenge now is how to replace your ounces for the future." The race to replace ounces is about to begin. It will take the form of takeovers of small producers with long reserve lives and high quality junior mining companies with large in ground reserves that can be mined economically."

People like Bobby Godsell publicly speaking about takeovers of high quality junior mining companies and Barrick tracking junior mining companies leads to only one single conclusion:

Juniors on the verge of Discovery will be in the spotlight soon!

So how to select a good junior explorer? Well, good question, ask 10 experts and you'll get 10 different answers, the only thing I can do is to share my thoughts on this.

First of all I like the junior explorers which survived the worst years of the bear market in Gold (Late 90's). This is important to me! Why? Because it tells me two important things:

- Those companies were and are true believers in Gold and its future potential. If they weren't, they would have quit the Gold market and transformed themselves into something else, into something fancy which was hot at that moment. Didn't we see many of the juniors making desperate moves and started financing all kind of E-commerce projects or other fancy hot-stuff? Well, we know the end result by now! For me it's quite simple. Most juniors without promising properties left the Gold arena in the late 90's, the ones with promising properties were hanging on and went into hibernation mode in order to survive. They did because they were/are true believers in Gold and its future potential and knew that hanging on would be rewarded somewhere in the nearby future.

- These companies are well run financially. So many juniors went bankrupt during the late 90's, only the ones with an iron financial discipline survived. So investing in a survivor makes me confident that management will spend my precious investment capital in a proper way!

The next step is to try to identify juniors with potential multi-million ounce deposits. This isn't easy, we investors aren't geologists, and we can't verify multi-million ounce deposit claims. Please be aware that only a very few multi million ounce Gold deposits do exist. According to Alex Davidson (Vice President Exploration Barrick) only three major deposits (5+ million ounce) have been discovered since 1999. So I would say select Junior Explorers with good Exploration Geologists with proven track records. Building a team of good Exploration Geologists requires good management. Therefore I consider good management as the greatest asset a Junior Explorer can have. A well managed company will find good properties.

So go for good management, but how you wonder? What is good management? Can you give me some characteristics of good management? Well, to be honest I can't! Yes, I can look at management's track-record as I've said before but just that single fact isn't sufficient for me to determine it's competence. In the end it's just a matter of trust and faith. Some people you trust and some you don't! Simple, it's all people business. So if I can't determine management's competence myself what should I do? Again, ask 10 experts and you'll get 10 different answers but again I'm happy to share my thoughts on this. Let's say you just spoke to a CEO of a junior mining company who says to be on the verge of a major discovery. It sounds good but you're wondering about the CEO's credibility. Let's say that this particular CEO was telling the truth, what do you think their shareholder base would look like? Wouldn't smart money already piled in you think? Don't you think that major producers would show some interest in this company for reasons well documented earlier? What I'm trying to say is that no matter what kind of potential discovery claims a junior makes, if it doesn't have a strong shareholder base I simply won't buy it. Even better, if you'll notice that some major producers took an interest in the company as well, which underscores of course the real possibility of finding major Gold Deposits. (I assume you agree with me that major producers aren't that stupid to invest in some empty drill holes with a liar on top of it)

I want to introduce a company right now that in my opinion meets the selection criteria mentioned above.

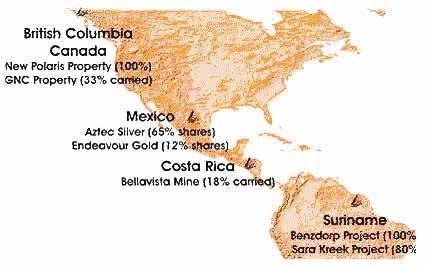

Canarc Resource Corp. (CCM.TO)Canarc Resource Corporation (TSX:CCM - OTCBB:CRCUF) is a growth-oriented gold exploration and mining company focused on building shareholder value through the discovery and development of large gold mines in North, Central and South America.

The Company owns interests in one small producing gold mine in South America, two large gold deposits ready for development in North and Central America, and several strategic exploration projects that have the potential for significant new mineral discoveries.

Canarc's New Polaris and Benzdorp projects in particular offer investors multi-million ounce gold potential. Most junior gold companies offer investors either production cash flow or a development opportunity or an exploration play. Canarc is unique in that is has all three: annual income, the largest undeveloped gold deposit in western Canada, and one of the most exciting exploration projects in South America.

A quick summary of Canarc's properties:

Benzdorp Property Suriname (80% option)

Benzdorp is historically the most prolific gold producing region in the Republic of Suriname with alluvial production exceeding 1 million oz. gold. Canarc recently announced an exciting new gold discovery on its Benzdorp property in Suriname. This target is a large, open pittable gold porphyry prospect with multi-million ounce potential.

Deposit Potential:

Several million oz. gold and several 100 million lbs copper geologically similar to the 10 million oz. Boddington mine in Australia (Newmont) and the 15 million oz. Cadia Hill deposit in Australia (Newcrest).

Current Status:

A 38 hole drill program has been completed on the JQA discovery area which has confirmed the existence of a large gold-copper porphyry deposit. An aggressive exploration drilling program is now underway to delineate an initial gold-copper resource in 2004. Management believes Benzdorp is potentially Canarc's next major gold discovery.

New Polaris BC Canada (100% Canarc)

A small high grade, underground past producing mine, New Polaris has become one of the largest gold deposits in Western Canada as a result of Canarc's successful exploration programs. The geological resource estimate is currently 1.3 million oz. (Not NI43-101 Compliant) at US $325 gold, but the mineralization is wide open along strike and at depth and could easily double with further drilling.

Deposit Potential:

Three million ounces plus, similar geologically to Placer Dome's Campbell Red Lake Mine (10 million oz.) high grade refractory ore body. Canarc's immediate goal is to develop a 700,000 oz. reserve suitable for a 600 ton per day mine, producing over 65,000 ounces of gold per year.

Current Status:

Polaris is an advanced stage exploration project, requiring infill drilling to further define proven and probable ore reserves followed by a full feasibility study. A scoping study is now underway to access the potential to develop a 65,000 oz. /year, over the next 3 years.

Bellavista Mine Costa Rica (18% Canarc)

Bellavista is a large, open pit, heap leach, epithermal gold deposit currently under construction. Canarc owns an 18% carried interest (after payback) and receives US$117,750 in annual preproduction cash payments.

Deposit Potential

1 million oz. plus, similar geologically to other volcanic-hosted epithermal gold deposits.

Current Status

The mine is currently under construction and Glencairn Gold Corp. anticipates its first gold pour by the end of 2004.

Endeavour Gold Corp. (EDR: TSX-V) (website) (Endeavour is an affiliate of Canarc, and Canarc has a significant shareholding (15%) and helps manage the affairs of EDR.)

Endeavour is a small-cap resource company focused on the discovery and development of high grade silver and gold mines in Mexico. With the recent acquisition of the Santa Cruz silver mine, Endeavour has become a new silver producer with extraordinary growth potential.

Deposit Potential

Great exploration potential is evidenced by a recent new discovery along strike from the mine and a historic paucity of exploration drilling. An independent report recently identified 2.8 million tonnes of potential ore reserves (not NI 43-101 compliant) in the SC vein, wide open along strike. The property covers over 3 km of known vein and the structure has been traced for more than 6 km.

Current Status

Endeavour is now targeting a 4-fold increase in production to1.8 million opy silver over the next year by developing the new discovery for mining. An additional rise in production up to 4 million opy silver is possible within three years by developing the other two known high grade ore shoots. That would make EDR a top 5 primary silver producer in North America.

Survivor of the worst bear market in Gold:

Canarc was founded 17 years ago by its CEO Brad Cooke. The worst years of the bear market in Gold (late 90's) weren't that pretty . So many juniors ended up with a less inspiring chapter 11 scenario and of course these dark days had its influence on Canarc as well. In order to survive Canarc virtually went into hibernation mode. Brad Cooke was determined in bringing Canarc through these dark days. Why? Simple! Because the properties Canarc owned would almost guarantee great upward potential for the company in a coming bull-market in Gold.

Management

As I've said before I consider management as one of the greatest assets a junior mining company can have. Here's what Jay Taylor (website) had to say about Canarc CEO Brad Cooke:

"Your editor (Jay Taylor) has known President, CEO and Director Brad Cooke since the early to mid 1980s. Nothing is more important than management and I believe Brad is about as capable as any junior mining company CEO you will find. Not only does he himself possess solid geological skills but he also has good business sense and people skills. As such he as assembled a team of competent folks around him.

Brad is a professional geologist, with more than 20 years of experience in geology and mineral exploration. He holds two university degrees in geology and has worked with the Ontario Department of Mines, Noranda, Shell and Chevron. Between 1983 and 1987 he owned and operated Cooke Geological Consultants, which found and developed several gold vein deposits for clients, and effectively reactivated interest in the Bralorne gold district -- historically, the largest gold producing region in British Columbia. In 1987, with the private management company ARC Resource Group, he founded Canarc and has overseen the growth of the company since that time, participating hands-on in the acquisition and exploration of strategic gold properties throughout the Americas."

END.

In an interview with Business TV on January 30 Jay Taylor said:

"I'm extremely bullish on Canarc...whenever I analyze Junior mining companies the first thing I look at is the management and as far as Canarc is concerned management is as strong as any junior company that I know of. I've known Brad Cooke since the early 1980's...he is a geologist, an honest man with great integrity in my view and he is very sharp in terms of finding out good properties and also selecting good people to work with him. Nothing is more important for any company than it's management whatever industry you are in...So overall, I think Canarc has the very very strong prospects of becoming a very successful mining company especially in light of a rising Gold price."

Interview can be watched at:

www.b-tv.com/i/videos/canarc.ram

END.

Shareholder Base

As mentioned earlier I consider a strong shareholder base as a must before I even start to think about investing in a junior mining company. Brad Cooke tells me that almost half of all Canarc shares are in strong hands. The list of shareholders is impressive and includes:

Barrick Gold

Kinross Gold

Another prominent supporter and shareholder of Canarc is Frank Veneroso.

Frank Veneroso is a highly esteemed financial market consultant of international stature. For those still unfamiliar with Frank Veneroso, here's a quick introduction:

Frank Veneroso is Market Strategist for the Global Policy Committee of Allianz Dresdner Asset Management and is responsible for alternative asset product development at Dresdner RCM. From 1991 to 1994 he was at the hedge fund Omega Advisors were he was the partner responsible for global investment policy formulation. From 1995 to 2000 and prior to 1991, through his own firm, Mr. Veneroso was an investment strategy advisor to global money managers and an economic adviser to institutions and governments around the world in the areas of money and banking, financial instability and crisis, privatization, and development and globalization of securities markets. His clients have included the World Bank, the International Finance Corporation, and The Organization of American States. He has advised the Governments of Bahrain, Brazil, Chile, Ecuador, Korea, Mexico, Peru, Portugal, Thailand, Venezuela and the United Arab Emerates. Frank is a graduate from Harvard and has authored many articles on the subjects of international finance.

Frank Veneroso runs the ABNAMRO Gold Certificate fund nowadays and also owns 'privately' a significant stake in Canarc.

Frank Veneroso has a good reputation of 'stock-picking'. Readers of LeMetropoleCafe know that Bill Murphy took a large holding in Golden Star Resources. Why? Because Frank Veneroso liked it! Here's what Bill Murphy had to say about Frank V.

"Golden Star Resources - My favorite gold stock and represents much of my gold share holdings. The reason is simple. It is Frank Veneroso's favorite gold stock. When I met Frank in 1980, he was best known as a Wall Street Whiz Kid stock picker. Frank has stated publicly that he believes that Golden Star is one of the most successful small gold exploration companies ever, having found 5 or 6 valuable properties in the Guyana Shield."

END.

Well, I don't think Bill Murphy has any regrets listening to Frank Veneroso regarding Golden Star Resources since it appreciated by more than 1200% since early 2001!

I think no further explanation is needed for reasons why I'm so excited to see Frank Veneroso as a major Canarc supporter.

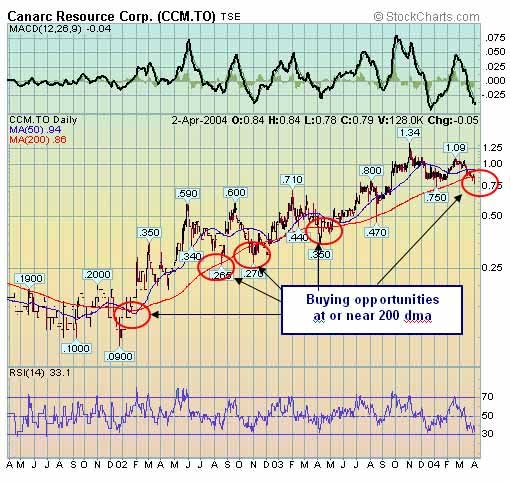

Canarc share price:

Canarc shares are trading currently for approximately CAD$0.90. It traded as high as CAD$1.30 last year. Does CAD$0.90 cents represents a good buying opportunity?

We already saw (on the HUI chart) that shares approaching the 200dma were presenting a good buying opportunity. So let's take a look the chart of Canarc itself and see where we are right now.

As said before, Junior shares tend to drop faster in a correction compared to their senior brothers. This is just a perfect example of what I mean, as we can see here Canarc shares are way oversold (shares hitting 200 dma, MACD and RSI indicator way oversold) and therefore represents imo a great buying opportunity at current levels (approx: 0.90 CAD$)

Canarc's future share price potential

OK, so if buying Canarc shares at current price levels represents a good buying opportunity what kind of share price seems to be reasonable within a year?

Well, that's almost impossible to say because a lot depends on the price of Gold. Although I strongly believe in higher prices for Gold next year this is not the main reason for investing in Canarc. As I said, the junior exploration sector is supported by two pillars, one is the price of Gold the other is declining Gold reserves. So if you're able to find a junior which is on the verge of discovery you will be rewarded anyhow, with or without higher Gold prices. I showed you the Victoria Resources example which share price doubled over night on Feb 26. Of course this hadn't anything to do with the price of Gold but rather with a good drill result!

The fact that Canarc is in my opinion on the verge of a major discovery on it's Benzdorp Property in Suriname South America can make Canarc a winner! CEO Brad Cooke makes a quick straight forward calculation, he says: " When you invest in Canarc you already own some real assets due to our 1.3 million ounce (Not NI43-101 Compliant) geological resource on our New Polaris property in BC Canada. These resource ounces alone already justify a share price of 1+ CAD$. So from an investors point of view you don't pay anything yet for all other Canarc properties including Benzdorp."

Canarc already mentioned that they believe to be on the verge of discovery of a multi-million ounce Gold deposit on its Benzdorp property. I asked Brad Cooke to be a bit more specific regarding which 'time-frame' he thinks Canarc can announce a new long awaited World Class Gold Deposit and its size.

Brad Cooke: " We're confident we have a new World Class Gold prospect with potential for 5 million ounces of Gold and we hope to make a definitive resource estimate before year end."

END.

Well, let's see, if 1.3 million ounces (Not NI43-101 Compliant) at the New Polaris property already justify a share price of 1+ CAD$, it ain't difficult to make an estimate for Canarc's share price at current Gold prices if they succeed in proving a 5 million ounce Gold deposit on its Benzdorp property in Suriname.

It's therefore my strong belief that once investors start to realize what kind of potential the Benzdorp property really has they will want to get in but it won't be that easy because half of all company shares are in strong hands.

Some smart market observers already took notice:

Jay Taylor - www.miningstocks.com

"The Benzdorp Could be a Monster Gold Deposit- The company's Benzdorp property, where the English and Dutch first mined gold in the late 1980s, is a huge claim area. There are four exploration concessions measuring 42 km x 31 km, totaling 138,000 hectares. Canarc holds an option to acquire a 100% interest (subject to a 20% NPI or 1% to 6% NSR) in the subsurface mineral rights from Grassalco, the state-owned mining company. Of course, more important than the size of the company's property are the prospects for discovering gold reserves. I believe the prospects for outlining one or more major gold deposits on the Benzdorp are excellent. . . Brad Cooke. . . noted that Canarc has already identified twelve gold targets, two of which are large tonnage gold/copper porphyry targets and the remaining ten are high-grade vein targets." - J.Taylor's Gold & Technology Stocks

END.

Small Cap Media reports:

Canarc's Drill Results Indicate Potential For A World-Class South American Gold Discovery.

END.

Chris Temple (2/18/04) - The National Investor:

"In my determination, Canarc is one company that the market place has generally not discovered.Valuations for some of the gold exploration companies touted the most aggressively in recent months remain rich (if not, in some instances, absurd) even after the latest correction in the sector. In Canarc's case, however, its valuation given the nature, potential and progress of its properties thus far is more like I'd have expected to see two years ago as this new metals bull market was getting started. Thus, it stands out as one we need to take a position in."

END.

Well, enough said regarding Benzdorp and its potential. The bottom line is this:

When you invest in Canarc you already own some real assets due to their 1.3 million ounce (Not NI43-101 Compliant) proven geological resource on the New Polaris property in BC Canada. With 56 million shares fully diluted and a price of approximately 0.90 CAD$ a share, the market values the known resources at New Polaris at a tiny $32 per ounce. Even at today's Gold price I consider this cheap. Think about it, you'll buy real assets for $32 per ounce Gold reserve and you'll get Benzdorp and Canarc's interest in Endeauvour Gold (12%) for free. Benzdorp hosts a potential new world class gold deposit while Endeauvour Gold has the potential to become a top 5 primary silver producer in North America. Still very few investors have picked upon it, hope you will!

Disclaimer:

The author maintains an investment position in Canarc and is not a professional investment advisor. Although this analysis is written upon request from Canarc the author hasn't been compensated upon his own request. This analysis is not a solicitation to buy or sell and no responsibility can be had for losses on the basis of this analysis. The reader should be aware that investing in Gold mining equities is a risky endeavor with a very real probability of substantial losses. Before making any investment decision, do your own research and consult a professional investment advisor.

Summary

High Quality Junior Exploration Companies will be in the spotlight soon due to:

- Gold price

- Declining Gold reserves

Gold Price:

We saw during 2001-2003 higher Gold prices lifting the entire Gold sector, so the big question remains:

"Has the bull market in Gold ended yet or has it hardly started?"

Jim Sinclair: I am a "believer" in the magnitude of the gold move that started at $342 and has had, as I have said often, a $480 plus number on it from the day it started.

Richard Russell: In the meantime, Russell advises subscribers to hold cash and gold, which, at $400 an ounce, is "as cheap as dirt." Eventually, he sees the yellow metal topping $1,000 an ounce -

Jim Puplava: The bull market in gold and silver has barely begun. It is still in its infancy as gold and silver move into their rightful role as real money.

Pierre Lassonde: Newmont president, Pierre Lassonde, is certain that the gold bull market remains in its infancy, and points investors to the 1970s to understand how events might unfold in gold's favour in an era of a "manic depressive dollar."

"We haven't even started to correct the US financial imbalance of the last three years. Don't tell me that the gold bull market is over. It has hardly even started," Lassonde told the audience at the 2004 BMO Nesbitt Burns Global Resources Conference in Tampa, Florida.

Declining Gold reserves:

Major producers will face a tremendous challenge in order to replace their dwindling Gold reserves. This is a direct result of the cut backs in Exploration budgets by 67% over the 1997-2002 period. Even with a Gold price of $1000, it still takes 4-7 years to open up a mine Pierre Lassonde (CEO Newmont Mining) said. Eventually the major producers will turn to the better Juniors with promising Gold properties in order to replace their depleted Gold reserves.

In his latest Essay "Open the Checkbooks - Buy the ounces" Jim Puplava of Financial Sense Online quoted Geologist H.R. Bullis who said:

"It is no longer a question of finding ounces anymore. It has become a question of survival.

According to geologist H.R. Bullis, today's VLGP's are unlikely to survive at current production rates over the next decade. It is time to open the checkbooks and go get the ounces."

We saw that the major Gold producers are facing a decline of ounces per share. That obviously means a decline in value as well. In order to compensate for this value-decline the producer needs a higher price of Gold. So investing in senior producers is betting on higher Gold prices. In other words, the only pillar carrying a major producer forward is a higher price of Gold!

So from an investors point of view it makes sense to invest in Junior Exploration companies with potential discoveries. Why? Simple! We saw how desperate the major producers are in order to replace their dwindling Gold reserves. We saw that new discoveries are rewarded tremendously by the market. So compared to their senior brothers the Juniors are being carried forward by two pillars instead of one.

END.

Please feel free to send comments at ehommelberg@planet.nl.

Eric Hommelberg

April 9, 2004

321gold Inc Miami USA